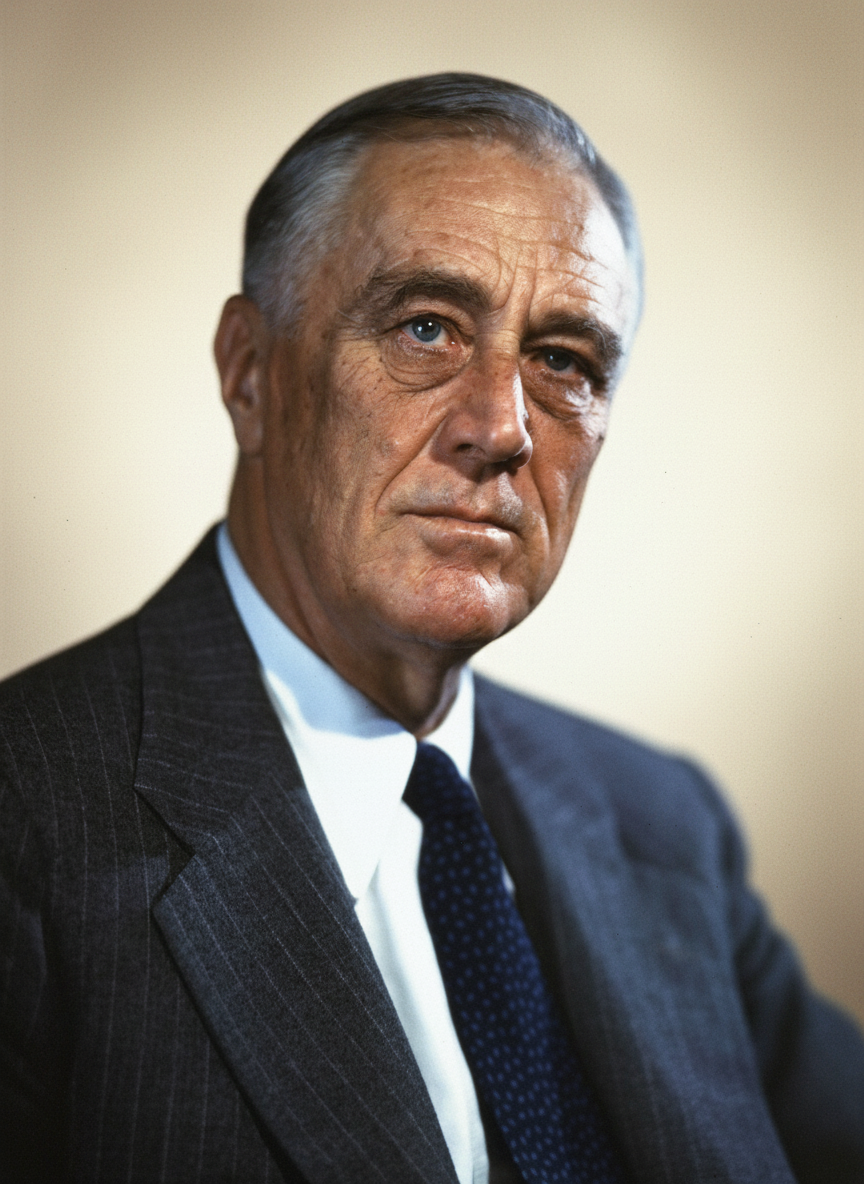

John Maynard Keynes

The architect of modern macroeconomics, whose theories profoundly reshaped governmental intervention in economic crises.

John Maynard Keynes was a British economist whose revolutionary theories challenged classical economics during the Great Depression. He advocated for government intervention, particularly through fiscal and monetary policies, to stabilize economies and combat unemployment, profoundly influencing post-war economic thought and policy.

Biography

Accomplishments

- 01Authored 'The General Theory of Employment, Interest and Money' (1936), which revolutionized macroeconomic theory and challenged classical laissez-faire economics.

- 02Central figure in the British Treasury during World War I and advisor on post-war reconstruction, deeply influencing national and international economic policy.

- 03Played a foundational role in the Bretton Woods Conference (1944), contributing to the establishment of the International Monetary Fund (IMF) and the World Bank.

- 04Developed the concept of the 'multiplier effect', explaining how initial changes in spending can have a magnified impact on national income.

- 05Articulated the 'liquidity trap,' a scenario where monetary policy becomes ineffective because interest rates are near zero and saving rates are high.

Lessons for Operators

Key Takeaways

Practical lessons distilled for operators, investors, C-levels, and capital allocators.

Aggregate Demand is King

Economic downturns are often a crisis of insufficient aggregate demand. Investment and consumption are primary drivers. Operators should focus on understanding consumer and business confidence, as these directly impact demand for their products and services.

Counter-Cyclical Policy Required

During recessions, governments should increase spending (fiscal stimulus) and lower interest rates (monetary stimulus) to offset falling private demand. Investors should anticipate such policies and position portfolios accordingly; C-levels should consider how government spending might create opportunities or mitigate risks for their sectors.

The Paradox of Thrift

While individual saving is prudent, if everyone saves excessively during a downturn, it collectively reduces aggregate demand, potentially worsening the recession. This implies that during certain market conditions, spending can be more economically beneficial than saving, a concept relevant to capital allocation strategies during crises.

Uncertainty's Impact on Investment

Investment decisions are significantly influenced by 'animal spirits'—waves of optimism or pessimism. High uncertainty reduces investment, hindering recovery. Leaders need to manage stakeholder expectations and foster environments that reduce perceived risk to encourage capital deployment.

Global Economic Interdependence

Keynes's post-war efforts at Bretton Woods emphasized the need for international economic cooperation and stable exchange rates. Global operators and investors must recognize that national policies have international ramifications, and vice-versa, influencing trade, capital flows, and market volatility.

Frameworks & Principles

Named frameworks and strategic principles they popularized or embodied.

Keynesian Aggregate Demand Model

This model posits that the total demand for goods and services in an economy (Aggregate Demand = C + I + G + (X-M)) is the primary determinant of overall economic activity and employment. Governments can influence these components (especially G - government spending) to stimulate growth.

When to useWhen analyzing economic downturns, understanding the root causes of unemployment (as demand-side rather than supply-side), and evaluating the potential impact of fiscal stimulus packages. Applicable for investors forecasting GDP, C-levels strategizing growth during recessions, and fund managers assessing market-wide demand.

The Multiplier Effect

An initial change in spending (e.g., government investment, consumer purchase) leads to a proportional, larger change in aggregate national income. The size of the multiplier depends on the marginal propensity to consume (MPC) and save (MPS).

When to useFor policymakers evaluating the effectiveness of stimulus measures, investors predicting the ripple effects of large infrastructure projects or tax cuts on economic sectors, and business leaders assessing the broader market impact of significant corporate investment or consumer trend shifts.

Liquidity Preference Theory

Keynes argued that people hold money for three motives: transactions, precautionary needs, and speculation. At very low interest rates, people may prefer to hold idle cash (liquidity trap) rather than invest in bonds, rendering monetary policy ineffective.

When to useRelevant for central bankers determining monetary policy strategies, investors understanding fixed-income market dynamics during periods of low interest rates, and financial advisors explaining why conventional monetary easing might not stimulate investment during severe downturns.

Sources & Further Reading

Profiles, interviews, podcasts, and articles used to compile and verify this entry. Each link opens at the original publisher.

Explore Related Titans

Other figures in the archive who share John Maynard Keynes's domain, geography, or era.

More in Other

From United Kingdom

Contemporaries — 19th century