Alfred Marshall

The architect of neoclassical economics, bridging classical thought and modern microeconomic analysis.

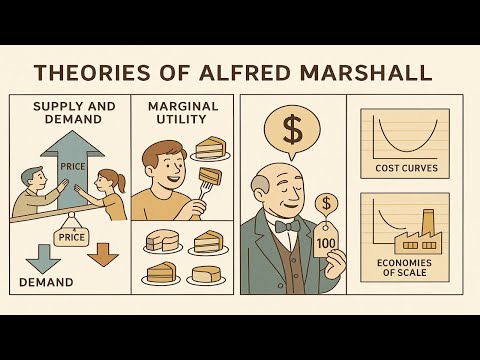

Alfred Marshall was a British economist who fundamentally shaped modern economic thought. His magnum opus, 'Principles of Economics' (1890), synthesized classical economics with new marginalist theories, establishing supply and demand, marginal utility, and elasticity as core concepts in microeconomics. He brought rigor and a practical focus to the discipline.

Biography

Accomplishments

- 01Authored 'Principles of Economics' (1890), which became the definitive economic textbook for decades, synthesizing classical and marginalist theories.

- 02Pioneered the concept of price elasticity of demand, providing a crucial tool for analyzing market responses to price changes.

- 03Introduced the analytical framework of supply and demand curves intersecting to determine market equilibrium, still foundational in microeconomics.

- 04Distinguished between short-run and long-run economic periods, enabling more nuanced analysis of production, costs, and market adjustments.

- 05Formally established economics as an independent academic discipline at Cambridge University, creating the first dedicated economics tripos (degree).

- 06Developed the concept of 'consumer surplus' and 'producer surplus,' providing a framework for welfare economics and policy analysis.

Lessons for Operators

Key Takeaways

Practical lessons distilled for operators, investors, C-levels, and capital allocators.

Integrated Market View

Successful strategy requires understanding the interplay of supply-side factors (costs, technology) and demand-side factors (consumer preferences, income) to determine equilibrium and competitive positioning. Avoid single-factor explanations for market dynamics.

Time-Phased Strategy

Distinguish between short-term tactical adjustments and long-term strategic investments. Different decisions yield different impacts over varying time horizons. Plan for both immediate responsiveness and enduring structural changes.

Data-Driven Pricing & Forecasting

Utilize elasticity concepts to quantify market sensitivity. Understand how changes in price, income, or substitute availability will affect demand for your products or investments, leading to more accurate revenue projections and pricing models.

Marginal Decision-Making

Decisions about scaling production, marketing spend, or adopting new technologies should focus on the incremental benefit versus incremental cost. Optimize at the margin for maximum efficiency and profitability, rather than relying on average costs or benefits.

Foundational Frameworks Endure

Marshall's fundamental concepts (supply/demand, elasticity, short/long run) remain indispensable tools for market analysis. Leaders must continuously leverage these core principles to diagnose market conditions and formulate robust strategies.

Frameworks & Principles

Named frameworks and strategic principles they popularized or embodied.

Supply and Demand Equilibrium

This framework posits that market prices and quantities are determined by the intersection of supply (the quantity producers are willing to offer at various prices) and demand (the quantity consumers are willing to buy at various prices). The equilibrium point represents the market clearing price and quantity.

When to useApplicable for analyzing any market, from commodities to labor. Use to understand price formation, predict the impact of policy changes (e.g., taxes, subsidies), or assess the influence of external shocks (e.g., supply chain disruptions, shifts in consumer preferences) on prices and sales volumes.

Price Elasticity of Demand/Supply

Measures the responsiveness of quantity demanded or supplied to a change in price. If elasticity is greater than 1, demand/supply is elastic (highly responsive); if less than 1, it's inelastic (less responsive).

When to useCrucial for pricing strategies: elastic demand suggests that price increases lead to significant revenue loss, while inelastic demand allows for price markups. For supply, it informs production planning and capacity expansion decisions. Use to optimize pricing, forecast revenue, and analyze competitive dynamics.

Short Run vs. Long Run

Distinguishes between periods where at least one factor of production is fixed (short run) and periods where all factors of production are variable (long run). In the short run, firms can adjust output by varying labor or materials; in the long run, they can change factory size, technology, or enter/exit the industry.

When to useEssential for strategic planning and investment appraisal. Use to understand cost structures (fixed vs. variable), evaluate investment decisions (e.g., building a new plant takes long-run planning), and analyze how firms adapt to market changes over different time horizons. Guides decisions on operational efficiency vs. strategic transformation.

Consumer Surplus & Producer Surplus

Consumer surplus is the difference between the maximum price consumers are willing to pay for a good and the actual market price. Producer surplus is the difference between the market price and the minimum price producers are willing to accept.

When to useApplicable for welfare analysis and policy evaluation. Use to understand the benefits derived by market participants, assess the efficiency of markets, and predict the impact of government interventions (e.g., price controls, taxes) on overall societal welfare and individual stakeholder value.

Recent Appearances

Latest interviews, keynotes, and press from the past half year.

youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.comyoutube.com

youtube.comyoutube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.comSources & Further Reading

Profiles, interviews, podcasts, and articles used to compile and verify this entry. Each link opens at the original publisher.

Explore Related Titans

Other figures in the archive who share Alfred Marshall's domain, geography, or era.

More in Other

From United Kingdom

Contemporaries — 19th century