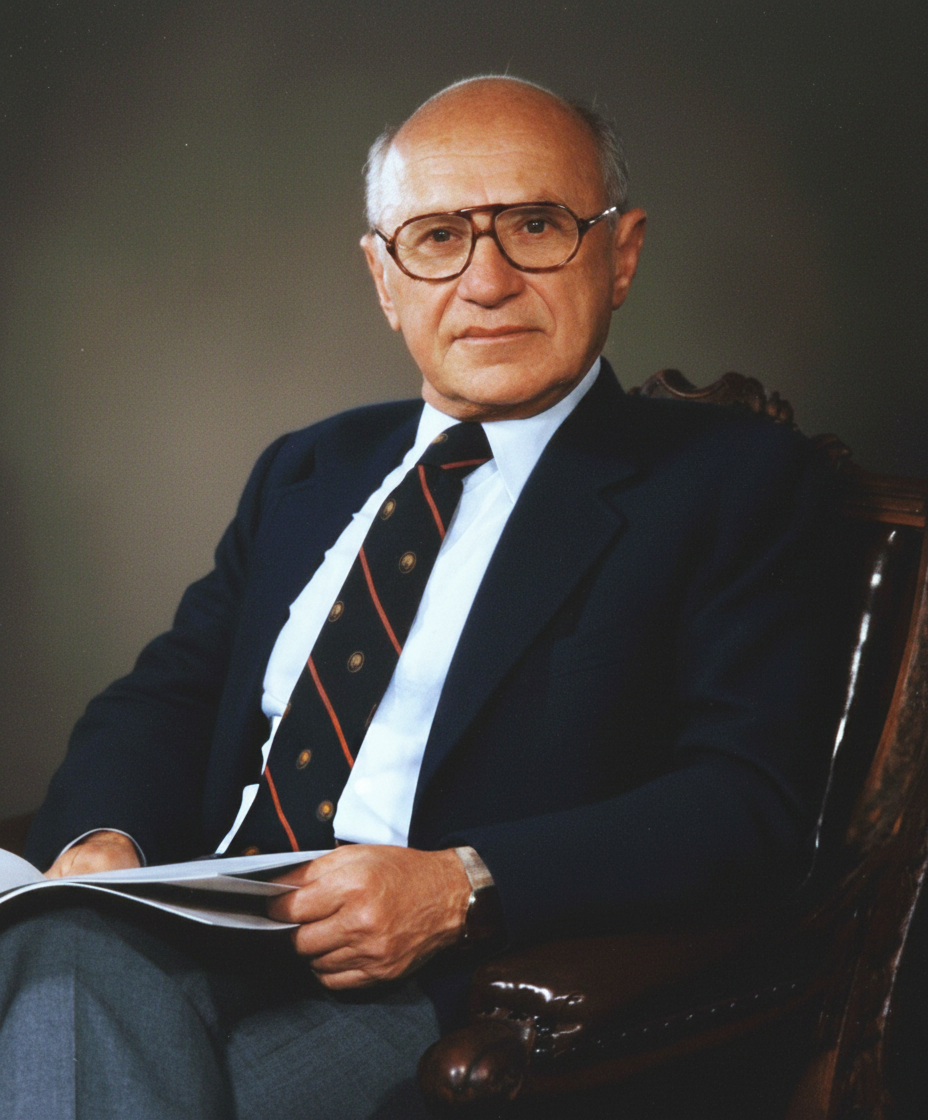

Milton Friedman

The intellectual architect of modern monetary policy and free-market capitalism.

Milton Friedman was a Nobel laureate economist known for his strong advocacy of free markets, limited government intervention, and his influential work on monetary theory. He challenged Keynesian economics, emphasizing the quantity of money as the primary determinant of inflation and business cycles.

Biography

Accomplishments

- 01Awarded the Nobel Memorial Prize in Economic Sciences in 1976 for his work on consumption analysis, monetary history and theory, and stabilization policy.

- 02Authored 'A Monetary History of the United States, 1867–1960' (1963) with Anna Schwartz, which fundamentally reshaped understanding of the Great Depression and the role of monetary policy.

- 03Led the intellectual shift from dominant Keynesian economic thought to monetarism, advocating for controlled money supply as the primary tool for economic stability.

- 04Influenced U.S. economic policy as an advisor to Presidents Nixon and Reagan, contributing to deregulation and monetarist approaches in the 1970s and 1980s.

- 05Pioneered the concept of the 'natural rate of unemployment,' arguing against the long-run Phillips Curve trade-off between inflation and unemployment, which became a cornerstone of modern macroeconomics.

- 06Founded the 'Chicago School of Economics,' a highly influential group advocating free-market principles, which produced numerous Nobel laureates and shaped global economic policy.

Lessons for Operators

Key Takeaways

Practical lessons distilled for operators, investors, C-levels, and capital allocators.

Money Matters Most

Friedman's central argument was that 'inflation is always and everywhere a monetary phenomenon.' Businesses must recognize the fundamental link between the money supply and price levels. For capital allocators, this means monitoring central bank policies is paramount, as excessive money growth will erode purchasing power and asset values over time. For operators, it underscores the need for sound pricing strategies that anticipate monetary shifts.

The Dangers of Discretionary Policy

He argued that government attempts to 'fine-tune' the economy often do more harm than good due to lags in data, policy implementation, and effect. This implies that businesses should prepare for economic volatility that policy interventions might exacerbate, rather than stabilize. Investors should be wary of political promises of perpetual stability, understanding that 'activist' government policies can introduce unpredictable risks.

Free Markets & Limited Government

Friedman championed individual economic freedom, arguing that competitive markets are the most efficient allocators of resources. For entrepreneurs and enterprise leaders, this means seeking out and thriving in environments with minimal regulatory burdens, strong property rights protection, and open competition. For investors, it suggests a preference for economies that adhere to these principles, as they tend to deliver sustainable long-term growth.

The Natural Rate of Unemployment

He posited that there's a 'natural rate' of unemployment determined by structural factors, and government attempts to push unemployment below this rate through monetary expansion will only lead to accelerating inflation without lasting employment gains. For C-levels and HR leaders, this perspective suggests focusing on improving workforce skills and structural efficiencies rather than relying on macroeconomic stimulus to solve deep-seated labor market issues. For policy advisors, it cautions against inflationary 'full employment' mandates.

Adaptive Expectations

Friedman's work highlighted how people and businesses adapt their expectations based on past experiences. If a central bank consistently prints money to stimulate demand, people will eventually expect inflation and adjust their behavior (e.g., demanding higher wages), making the policy ineffective in real terms. Operators must anticipate how their stakeholders (employees, customers, suppliers) will react to perceived policy shifts, baking these 'adaptive expectations' into strategic planning and pricing.

Frameworks & Principles

Named frameworks and strategic principles they popularized or embodied.

Quantity Theory of Money (QTM)

Expressed by the equation MV=PQ (Money Supply x Velocity of Money = Price Level x Real Output), this theory posits that in the long run, and assuming velocity and real output are relatively stable, changes in the money supply directly lead to proportional changes in the price level (inflation). Friedman updated this by emphasizing the demand for money and linking it to permanent income.

When to useApplicable when forecasting long-term inflation trends, understanding the impact of central bank quantitative easing/tightening, or evaluating the purchasing power erosion on long-term investments. Businesses use it to inform long-range financial planning and pricing strategies.

Permanent Income Hypothesis

Consumers base their consumption decisions not on their current annual income, but on their 'permanent income' – their expected long-term average income. This implies that temporary changes in income have little effect on consumption, while permanent changes have a larger impact.

When to useUseful for businesses predicting consumer spending patterns and market demand in response to policy changes (e.g., temporary tax cuts vs. permanent wage increases). Investors can use it to understand consumer resilience during short-term economic shocks.

Monetary Rule (K-Percent Rule)

Friedman advocated for a fixed monetary rule, where the central bank would increase the money supply annually by a constant percentage (e.g., 3-5%), roughly equal to the long-term growth rate of real GDP. This rule aimed to eliminate discretionary monetary policy and provide stable prices.

When to useWhile not widely adopted as a strict rule, the principle is relevant for investors assessing central bank credibility and predictability. Businesses can use it to advocate for stable, non-discretionary monetary policy from governments, reducing uncertainty in long-term capital investments.

Sources & Further Reading

Profiles, interviews, podcasts, and articles used to compile and verify this entry. Each link opens at the original publisher.

Explore Related Titans

Other figures in the archive who share Milton Friedman's domain, geography, or era.

More in Other

From United States

Contemporaries — 20th century