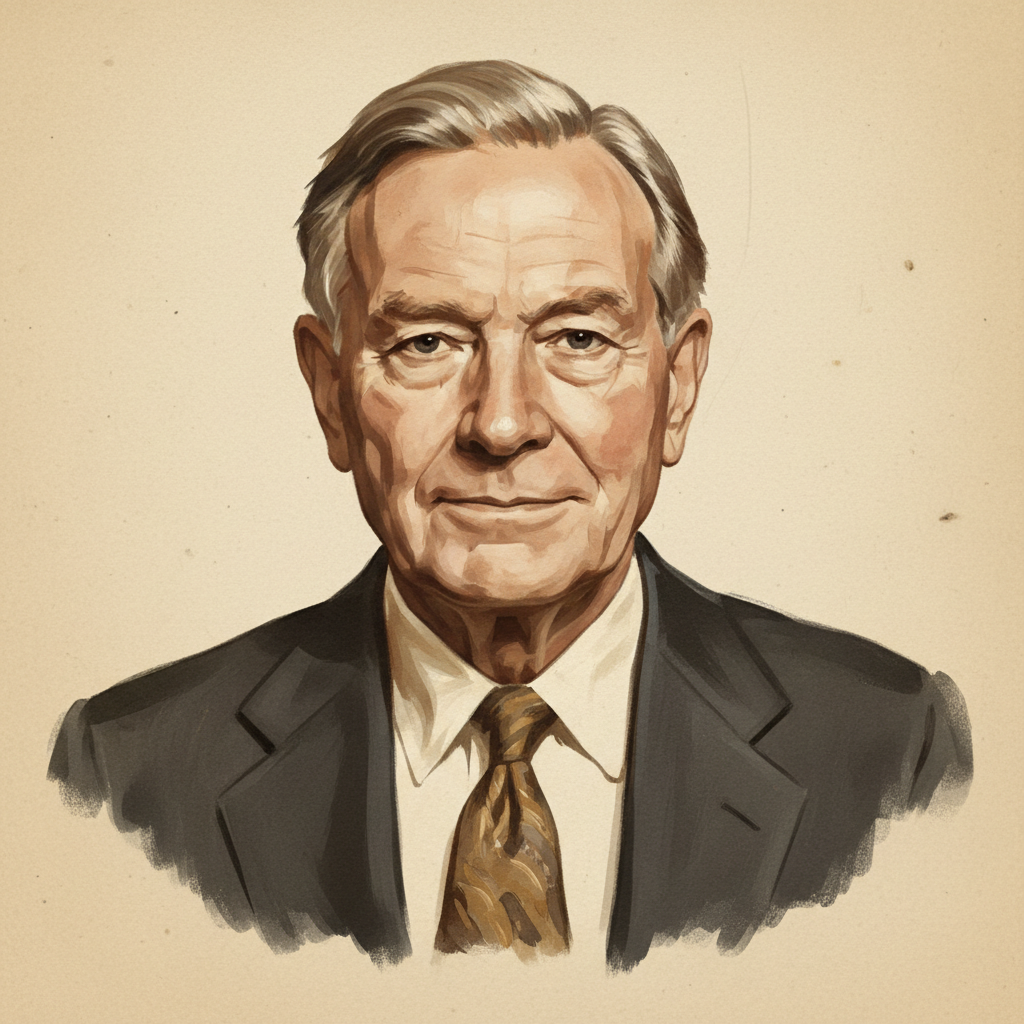

Alan Greenspan

The Maestro who navigated the US economy through two decades of volatility and unprecedented growth.

Alan Greenspan served as Chairman of the Federal Reserve from 1987 to 2006, leading the U.S. central bank through periods of significant economic change, including the 1987 stock market crash, the dot-com bubble, and the early years of the 21st century housing boom. His tenure was marked by a pragmatic, data-driven approach to monetary policy.

Biography

Accomplishments

- 01Successfully navigated the 1987 stock market crash ('Black Monday') through swift action, ensuring market liquidity and confidence, preventing a wider financial collapse.

- 02Presided over 'The Great Moderation' (mid-1980s to 2007), a period of significantly reduced macroeconomic volatility, characterized by stable inflation and sustained economic growth.

- 03Managed the unwinding of the dot-com bubble in 2000-2001 with a series of interest rate cuts, aiming for a 'soft landing' for the economy.

- 04Led the Federal Reserve's response to the September 11, 2001, terrorist attacks, implementing interest rate cuts to stabilize financial markets and prevent a recession.

- 05Oversaw the transition to explicit inflation targeting by central banks globally, influencing monetary policy frameworks beyond the United States.

Lessons for Operators

Key Takeaways

Practical lessons distilled for operators, investors, C-levels, and capital allocators.

Central Bank Independence is Crucial

Greenspan's ability to make difficult policy decisions, often under political pressure, underscored the importance of central bank independence for long-term economic stability. For businesses, this translates to insulating critical decision-making bodies (e.g., R&D, capital allocation) from short-term political or internal pressures to ensure a focus on long-term value.

The 'Greenspan Put' and Moral Hazard

The perception that the Fed would intervene to mitigate significant market downturns (the 'Greenspan Put') arguably fostered excessive risk-taking. While central bank intervention is necessary in crises, businesses should avoid operating under the assumption of a 'bailout' and instead build robust risk management and capital structures to weather downturns independently.

Risk of Asset Bubbles in Low-Interest Rate Environments

Greenspan's extended period of low interest rates, particularly after 9/11, is often cited as a contributing factor to the housing bubble. Investors and allocators must be acutely aware that prolonged low-rate environments can inflate asset prices disproportionately to fundamentals, demanding heightened scrutiny of valuations and judicious capital deployment.

Credibility as a Monetary Policy Tool

Greenspan's personal credibility and the Fed's institutional credibility were powerful tools for influencing market expectations and steering the economy. For C-levels, building and maintaining organizational credibility through consistent performance, transparent communication, and ethical conduct is an invaluable asset in managing stakeholder relationships and market perception.

The Imperative of Liquidity Management

His immediate response to the 1987 crash focused on ensuring market liquidity. This highlights that access to ample liquidity, especially during stress events, is non-negotiable for financial stability. Businesses must maintain adequate cash reserves, credit lines, and diversified funding sources to withstand unforeseen shocks.

Frameworks & Principles

Named frameworks and strategic principles they popularized or embodied.

Greenspan's Risk Management Approach

Greenspan's philosophy involved proactively addressing perceived risks to economic stability, often by 'erring on the side of caution' concerning inflation or by swift liquidity injections during market crises. He emphasized identifying emerging imbalances and taking preventative measures.

When to useApply when analyzing systemic risks within an industry or economy. Operators should adopt a 'precautionary principle' for critical business functions, preemptively addressing potential failures in supply chains, cybersecurity, or financial solvency rather than reacting after a crisis.

The 'New Economy' Paradigm

Greenspan acknowledged the structural shift towards a 'new economy' driven by information technology, which he believed reduced inflationary pressures by increasing productivity. This informed his willingness to allow the economy to grow faster than traditional models might suggest without raising rates too aggressively.

When to useRelevant when assessing the impact of new technologies on productivity, cost structures, and market dynamics. Investors and C-levels should actively research and understand how technological advancements are fundamentally altering industry landscapes, potentially disrupting old rules of thumb for growth, profitability, and competitive advantage.

Dynamic Monetary Policy (vs. Rules-Based)

Greenspan largely favored a discretionary, data-dependent approach to setting interest rates and managing the money supply, rather than strictly adhering to predetermined rules (like the Taylor Rule). This allowed for greater flexibility in responding to evolving economic conditions.

When to useApplicable for strategic decision-making in highly dynamic markets. Rather than rigid long-term plans, enterprise leaders should cultivate agile strategies that allow for rapid adjustments based on real-time market feedback, competitive actions, and macroeconomic shifts. This requires strong data analytics capabilities and a culture of adaptability.

Recent Appearances

Latest interviews, keynotes, and press from the past half year.

youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.com youtube.com

youtube.comSources & Further Reading

Profiles, interviews, podcasts, and articles used to compile and verify this entry. Each link opens at the original publisher.

Explore Related Titans

Other figures in the archive who share Alan Greenspan's domain, geography, or era.

More in Finance & Investing

From United States

Contemporaries — born 1920s