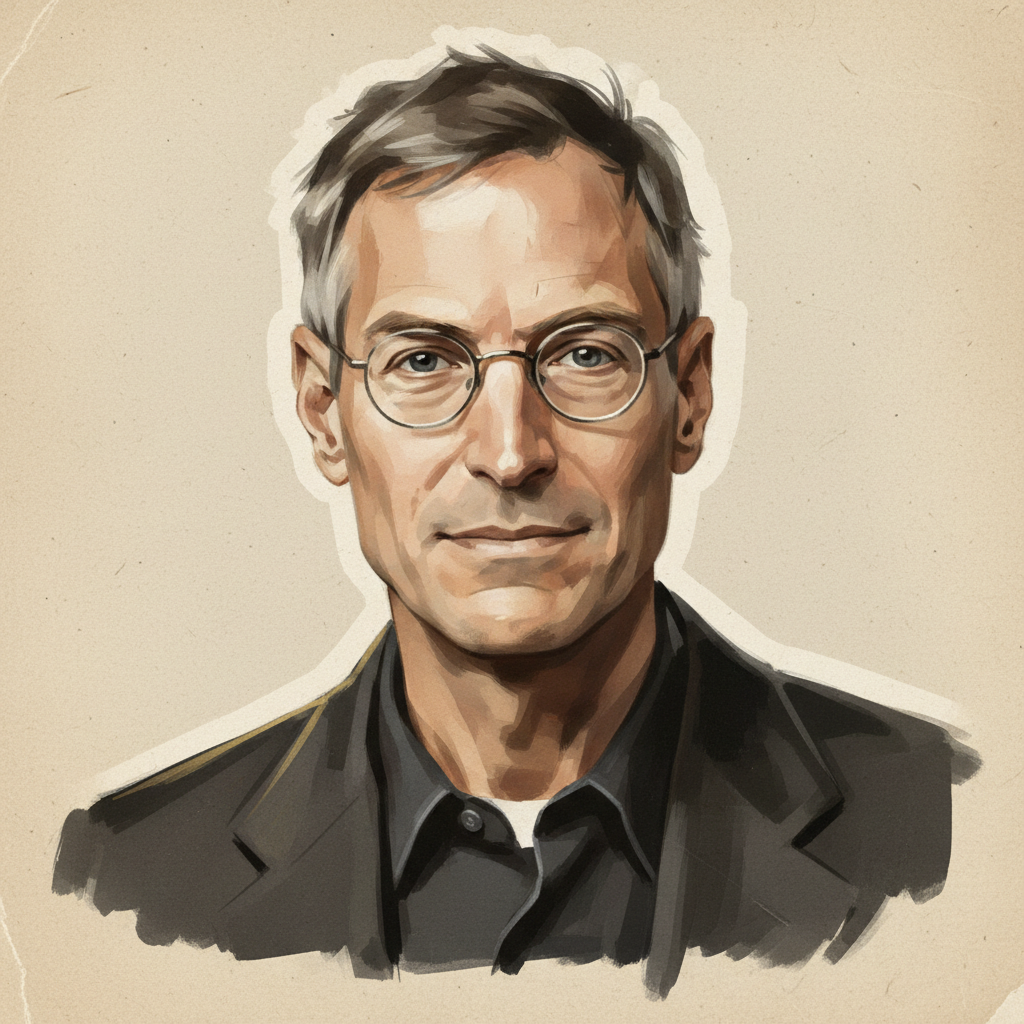

Seth Klarman

The 'Oracle of Boston,' renowned for value investing, risk aversion, and independent thought in managing capital.

Seth Klarman is an American billionaire investor, hedge fund manager, and author. He is the founder and CEO of The Baupost Group, a Boston-based private investment partnership founded in 1982. Known for his deep value investing approach, Klarman often invests in out-of-favor securities, distressed debt, and complex situations, emphasizing risk management and capital preservation.

Biography

Accomplishments

- 01Founded The Baupost Group in 1982, transforming it into one of the largest and most successful hedge funds globally, consistently generating strong, risk-adjusted returns for over four decades.

- 02Authored 'Margin of Safety: Risk-Averse Value Investing Strategies for the Thoughtful Investor' (1991), a seminal work in value investing, which remains highly influential and sought after due to its practical insights.

- 03Successfully navigated numerous market crises, including the Dot-com bubble (2000-2002), the 2008 financial crisis, and the COVID-19 pandemic, by prioritizing capital preservation and opportunistic buying.

- 04Achieved an annualized return often cited in the high teens since inception, significantly outperforming broader market indices with lower volatility.

- 05Managed a substantial portion of assets in cash during periods of perceived overvaluation, demonstrating conviction and discipline in capital allocation, such as holding over 30% cash in 1999 and again preceding the 2008 crisis.

- 06Invested in complex and unconventional opportunities, such as distressed debt of companies like Enron post-bankruptcy, subprime mortgage-related securities during the 2008 crisis, and long-term positions in publicly traded companies like eBay (EBAY) and Liberty Global (LBTYA).

Lessons for Operators

Key Takeaways

Practical lessons distilled for operators, investors, C-levels, and capital allocators.

Rigorous Value Investing

Klarman's approach is deeply rooted in Benjamin Graham's value investing principles. This involves buying assets for less than their intrinsic value, creating a 'margin of safety.' He applies this across asset classes, including public equities, distressed debt, real estate, and private businesses. For instance, Baupost purchased distressed real estate during the early 1990s recession and again after the 2008 financial crisis.

Patience and Opportunism

Klarman is renowned for his willingness to hold large cash positions (sometimes over 30% of AUM) for extended periods when attractive opportunities are scarce. He views cash not as a drag but as a call option on future attractive investments, allowing Baupost to deploy capital aggressively during market panics or dislocations. This was evident during the COVID-19 market sell-off in early 2020, when Baupost actively deployed capital.

Risk Aversion and Capital Preservation

Risk management is paramount. Klarman focuses on downside protection, emphasizing that 'losing money is a bigger deal than making money.' He avoids permanent capital impairment and seeks investments where the potential for loss is limited, even if the upside is also constrained. This mindset differentiates him from many growth-focused fund managers.

Independent and Contrarian Thinking

Klarman avoids following the crowd, often investing in out-of-favor sectors or complex securities that others shun. He believes that true opportunities often arise from fear, uncertainty, and illiquidity, where deep fundamental analysis can uncover mispriced assets. His firm has been known to invest in sectors like telecommunications (e.g., Sprint Nextel debt) when they were experiencing significant turmoil.

Complexity as an Edge

The Baupost Group actively seeks out complex, illiquid, or niche investments that often require significant research and legal expertise. These situations, such as bankruptcy reorganizations, spin-offs, or regulatory changes, tend to be less efficient and thus offer better pricing. This approach often leads them into distressed debt markets, where they can influence outcomes or secure favorable terms.

Frameworks & Principles

Named frameworks and strategic principles they popularized or embodied.

Margin of Safety

Investing at a significant discount to intrinsic value to protect against unforeseen adversities, errors in judgment, or economic downturns. This provides a 'cushion' against permanent capital loss.

When to useApplicable to all investment decisions, especially when evaluating equities, bonds, or real estate. Essential during periods of market uncertainty or when targeting long-term capital preservation.

Opportunistic Cash Holdings

Deliberately holding significant cash reserves even during bull markets. This strategy forgoes immediate returns but positions the investor to deploy capital aggressively when market dislocations or attractive values emerge.

When to useEmploy this strategy when market valuations appear stretched, high-quality investment opportunities are scarce, or during periods preceding anticipated economic downturns like the 2008 crisis or early 2020.

Deep Value/Distressed Investing

Focusing on severely undervalued or financially distressed assets, often in complex situations like bankruptcy, reorganization, or out-of-favor industries. This requires extensive due diligence and often involves active engagement with companies or creditors.

When to useStrategic during bear markets, sector-specific downturns, or when individual companies face temporary but resolvable financial distress. Requires expertise in legal structures and financial restructuring.

Bottom-Up Fundamental Analysis

Thoroughly researching individual companies, industries, and asset classes to understand their intrinsic worth, independent of market sentiment. This involves analyzing financial statements, competitive landscapes, management quality, and future prospects.

When to useCrucial for all investment decisions, especially when identifying intrinsic value for the Margin of Safety framework. Essential before committing capital to any investment, regardless of market conditions.

Sources & Further Reading

Profiles, interviews, podcasts, and articles used to compile and verify this entry. Each link opens at the original publisher.

Explore Related Titans

Other figures in the archive who share Seth Klarman's domain, geography, or era.

More in Finance & Investing

From United States

Contemporaries — born 1950s