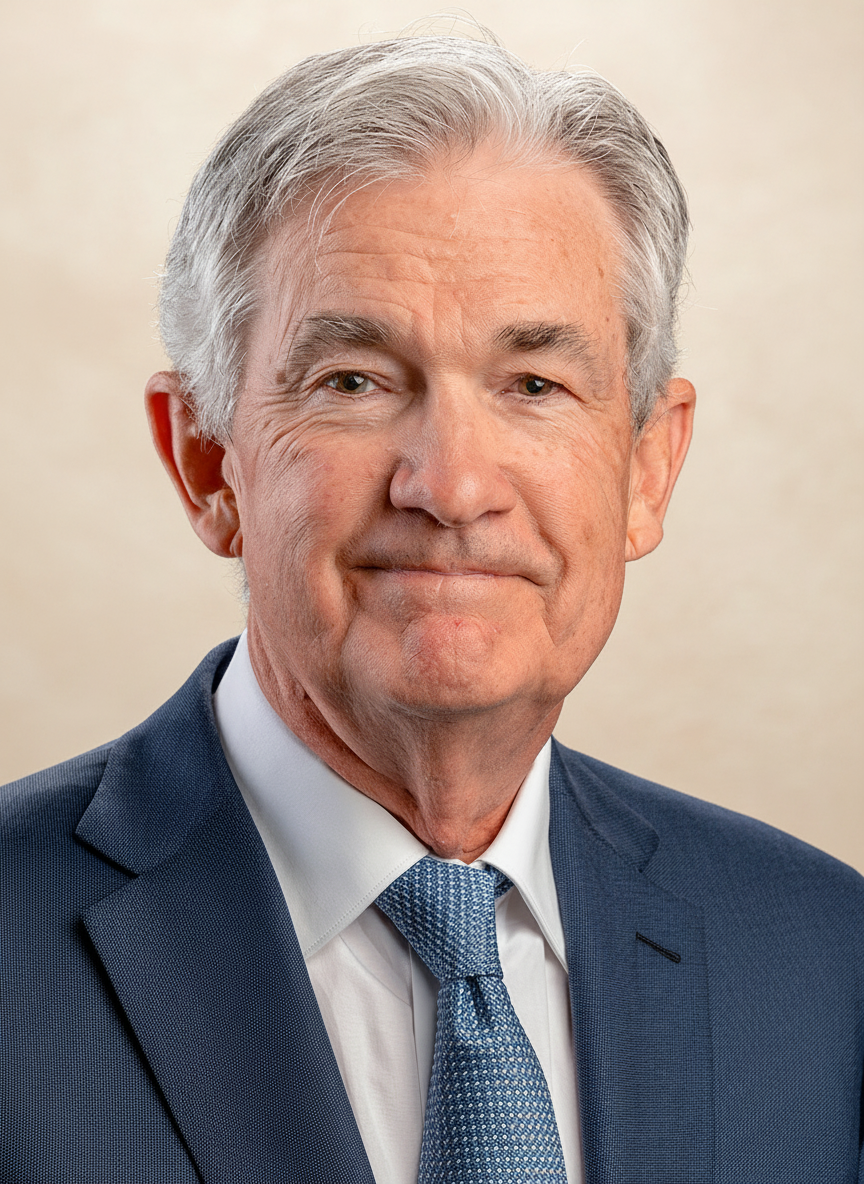

Jerome Powell

The Maestro of Monetary Policy: Navigating Economic Headwinds and Shaping the Federal Reserve's Modern Era

Jerome Hayden "Jay" Powell is an American central banker and attorney who served as the 16th chair of the Federal Reserve from 2018 to 2026. He previously held roles as both a lawyer and investment banker in the private sector before committing to public service.

Biography

Accomplishments

- 01Steered U.S. monetary policy through the unprecedented economic crisis induced by the COVID-19 pandemic, implementing aggressive quantitative easing and near-zero interest rates to stabilize markets and support economic recovery.

- 02Oversaw the Federal Reserve's review of its monetary policy framework, culminating in a shift to 'flexible average inflation targeting' in August 2020, aiming for inflation to average 2% over time, allowing for periods of overshoot after undershoots.

- 03Initiated the first rate hike cycle since 2018, beginning in March 2022, to combat persistent inflation, demonstrating a commitment to price stability even amidst global economic uncertainties.

- 04Managed robust economic growth and historically low unemployment rates during his early tenure (2018-2019), navigating trade tensions and global growth concerns without significant economic disruption.

- 05Successfully addressed market liquidity crises, most notably in March 2020, through emergency lending facilities and asset purchases, preventing a more severe financial meltdown.

Lessons for Operators

Key Takeaways

Practical lessons distilled for operators, investors, C-levels, and capital allocators.

Crisis Management Expertise

Powell's tenure highlights the critical role of central bank leadership in providing stability during extreme economic dislocations. His decisive actions in 2020 averted a deeper crisis, showcasing the power of rapid, broad-based monetary intervention.

Evolution of Monetary Policy

The Federal Reserve's shift to flexible average inflation targeting under Powell signals a sustained commitment to allowing the economy to 'run hot' for periods to foster maximum employment, moving away from pre-emptive tightening based on inflation forecasts alone. Investors and operators must understand this nuanced approach.

Balancing Dual Mandate

Navigating both maximum employment and price stability mandates requires constant recalibration. Powell's Fed demonstrated a willingness to prioritize employment during the pandemic recovery, then aggressively address inflation, illustrating the dynamic tension and trade-offs inherent in central banking.

Communication as a Policy Tool

The clarity and consistency of central bank communication are almost as important as the policy decisions themselves. Powell's direct engagement with the public and markets has been crucial in anchoring expectations and fostering confidence.

Private Sector Acumen in Public Service

Powell's background in investment banking provided a practical understanding of financial markets, corporate balance sheets, and real-world capital allocation, which proved invaluable in formulating responses to financial crises and understanding the transmission mechanisms of monetary policy.

Frameworks & Principles

Named frameworks and strategic principles they popularized or embodied.

Flexible Average Inflation Targeting (FAIT)

A monetary policy framework where the central bank aims for inflation to average 2% over time, meaning it may allow inflation to run moderately above 2% for some time following periods when it has run persistently below 2%.

When to useApplicable for central banks seeking to enhance the credibility of their 2% inflation target, particularly after prolonged periods of undershooting, thereby supporting maximum employment and avoiding disinflationary traps.

Forward Guidance

A communication strategy where the central bank provides signals about the future path of monetary policy, such as interest rates or quantitative easing, based on specific economic conditions or forecasts.

When to useUtilized by central banks to manage market expectations, increase transparency, and enhance the effectiveness of monetary policy, especially in periods where the policy rate is constrained by the effective lower bound.

Quantitative Easing (QE) and Tightening (QT)

QE involves large-scale asset purchases (e.g., government bonds, mortgage-backed securities) by the central bank to lower long-term interest rates and increase money supply. QT is the reverse, involving the reduction of the central bank's balance sheet.

When to useQE is employed to provide monetary stimulus when policy rates are at their effective lower bound. QT is used to normalize monetary policy and reduce excess liquidity when inflation is a concern or the economy is robust.

Sources & Further Reading

Profiles, interviews, podcasts, and articles used to compile and verify this entry. Each link opens at the original publisher.

Explore Related Titans

Other figures in the archive who share Jerome Powell's domain, geography, or era.

More in Finance & Investing

From United States

Contemporaries — born 1950s