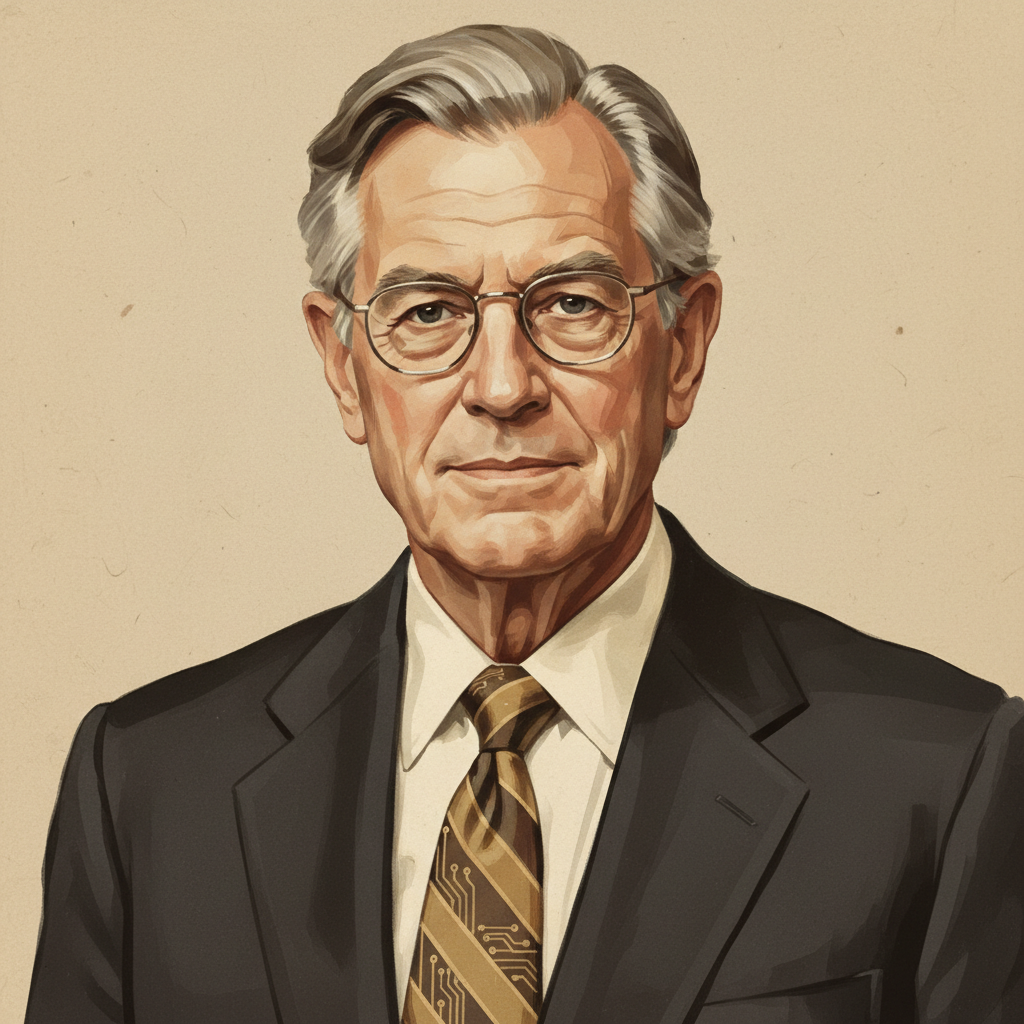

Howard Marks

Co-founder of Oaktree Capital Management, prominent investor, and author known for 'The Most Important Thing'.

Howard Marks is an American investor, writer, and fund manager. He is the co-founder and co-chairman of Oaktree Capital Management, a leading global investment firm specializing in alternative investments. Marks is renowned for his insightful memos to clients, which distill complex investment principles into actionable wisdom, and his influential book, 'The Most Important Thing: Uncommon Sense for the Thoughtful Investor'.

Biography

Accomplishments

- 01Co-founded Oaktree Capital Management in 1995, which grew into a global investment firm with over $170 billion in assets, specializing in alternative investments like distressed debt.

- 02Authored 'The Most Important Thing: Uncommon Sense for the Thoughtful Investor' (2011), a seminal work on investment philosophy widely praised by industry leaders.

- 03Developed and disseminated a unique investment approach emphasizing second-level thinking, understanding cycles, and managing risk, articulated through his widely read client memos (starting 1990).

- 04Successfully navigated multiple market cycles, including the dot-com bubble (2000), the subprime mortgage crisis (2008), and the COVID-19 pandemic (2020), demonstrating consistent long-term success in credit and distressed debt markets.

- 05Led TCW Group's high-yield bond, convertible securities, and distressed debt efforts from 1985 to 1995, achieving significant returns during a period of market expansion.

Lessons for Operators

Key Takeaways

Practical lessons distilled for operators, investors, C-levels, and capital allocators.

The Power of Second-Level Thinking

Most investors stop at first-level thinking (e.g., 'Company X is good, so buy its stock'). Marks advocates for second-level thinking: 'Company X is good, but everyone thinks it’s good, so the stock is overpriced, therefore I won't buy it.' This deeper analysis identifies mispriced assets by considering the consensus view and potential deviations.

Mastering Market Cycles

Markets move in cycles driven by human psychology, risk tolerance, and economic conditions. Operators and investors must understand where they are in the current cycle (e.g., euphoria, fear, recovery) to position portfolios defensively or aggressively. Successful capital allocators exploit extremes, buying when pessimism is high and selling when optimism peaks.

Risk Management as the Linchpin

Marks asserts that controlling risk is paramount, as return will follow. This means carefully assessing downside potential, avoiding permanent loss of capital, and building portfolios with buffers. His emphasis on distressed debt stems from the belief that investing in 'broken' but fundamentally sound companies at low prices offers a margin of safety.

Value Creation in Distressed Assets

Oaktree's core strategy involves investing in distressed debt and credit opportunities. This involves acquiring debt instruments of financially troubled companies at a discount, then either restructuring the debt, taking equity control, or benefiting from the company's turnaround. This strategy requires deep due diligence and a long-term perspective.

The Importance of Behavioral Finance

Marks frequently highlights how investor psychology—greed and fear—drives market extremes. Recognizing and counteracting these emotional biases (e.g., not buying into hype, not panicking during downturns) is critical for achieving superior returns. Rational contrarianism is a result of understanding these behavioral patterns.

Frameworks & Principles

Named frameworks and strategic principles they popularized or embodied.

Second-Level Thinking

Moving beyond initial, superficial conclusions to consider 'the consensus' and how one's own assessment differs and why. It involves thinking about the implications of the implications.

When to useApplicable in any decision-making process, particularly in competitive environments such as investment allocation, strategic planning, or product development, where outperforming the average requires a non-consensus, yet correct, view.

Market Cycle Awareness

A framework for understanding that markets and economies move in predictable but not precisely timeable cycles (e.g., boom-bust, expansion-contraction). It emphasizes assessing where one is in the cycle to adjust strategy.

When to useEssential for capital allocators, portfolio managers, and C-level executives when setting long-term strategy, making significant capital expenditures, or adjusting risk exposure in their businesses or investments. It informs when to be aggressive versus defensive.

Risk Control as Return Driver

The philosophy that superior long-term returns are best achieved by assiduously avoiding significant losses rather than aggressively seeking outsized gains through elevated risk. It prioritizes downside protection.

When to useCritical for all forms of prudent management. Fund managers planning portfolio construction, CFOs managing corporate balance sheets, or entrepreneurs launching ventures should prioritize identifying and mitigating potential failure points over solely focusing on upside potential.

Sources & Further Reading

Profiles, interviews, podcasts, and articles used to compile and verify this entry. Each link opens at the original publisher.

Explore Related Titans

Other figures in the archive who share Howard Marks's domain, geography, or era.

More in Finance & Investing

From United States

Contemporaries — born 1940s